Microsoft (MSFT)

Microsoft remains a favourite here at WSX thanks to its cash flows, high earnings growth forecasts and reasonable valuation at a 26 PE. MSFT stock has beat all 4 of its last earnings calls and analysts are rating it a Strong Buy with an average one year forecast of +32%. While they are increasing exposure to new technologies like AI they also have plenty of dependable cash producing services like Azure and Office 365 which they are likely keen on integrating with any optimization AI has to offer. We have put them as low risk, medium reward and have rated it a Strong Buy with a +17% one year forecast.

Taiwan Semiconductor (TSM)

At a 34 PE, TSM is an incredible bargain that is looking to improve their EPS from $9.53 TTM to $14.37 by the end of the year – and incredible 50% forecasted increase. Assuming the share price remains the same over that time, that would give TSM a PE of 17 which is much too low given a company of this nature; meaning the share price would have to go up if it can meet that 50% EPS growth target by the end of December. We think this is likely as TSM has beat all 4 of their last earnings calls and continues to log strong revenue growth. We put TSM as a medium risk, high reward stock and have it rated it a Strong Buy with a +18% one year forecast.

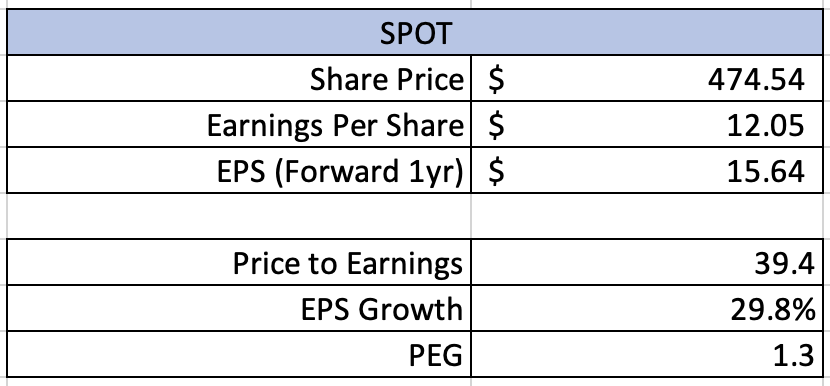

Spotify (SPOT)

Down over 33% this past 6 months, SPOT stock has come a long ways off its mid-2025 highs despite earnings upgrades and impressive user base growth. Now with over 626M users, around 7.5% of the world’s entire population are considered users of Spotify. SPOT is expected to improve its EPS by around 29% this year, giving it a respectable PEG of 1.3 given its industry. And while they have only beat their latest 2 earnings calls, we put Spotify as a medium risk, high reward stock and have it rated it a Strong Buy with a +13% one year forecast.